Probably like you, we’re hearing the dreaded “R” word – recession – being referenced quite a bit lately.

In fact, in the month of June, Google Trends – which analyzes the popularity of Google Search across various regions and languages – indicated that searches for “recession” have officially surpassed those for “inflation.”

What’s causing the dim outlook?

In simplest terms: Uncertainty.

Most of that uncertainty lands squarely around the recently overtaken Google Search favorite: inflation.

At the European Central Bank Forum in Sintra, Portugal last week, Fed Chair Jerome Powell – the man with quite possibly the most unenviable job in America right now – said:

“I think we now understand better how little we understand about inflation” and that there is “no guarantee the central bank can tame runaway inflation without hurting the job market.”

Not the most reassuring words.

Inflation Blame

A succinct summary of inflation contributors (credit to Barry Ritholtz):

- Covid-19

- Congress

- President Biden CARES Act 3

- President Trump CARES Act 2

- Consumers (who overspent without regard to cost)

- Consumers (shift to goods)

- Russian invasion of Ukraine

- Just In Time Delivery (supply chain)

- Fed/Monetary Policy

- Wages/Unemployment Insurance

- Home Shortages

- Semiconductors/Automobiles

- Corporate Profit Seeking

- Tax Cuts (2017) / Infrastructure (2022)

- Crypto

Inflation: The Path Forward

Between a rock and a hard place, the Fed has made clear that it will prioritize reining in inflation.

To do this, the Fed will continue tightening monetary policy. Quantitative easing (QE discussed more in previous contribution) has been discontinued and additional interest rate increases are planned.

The question then becomes – as Powell alluded to in Sintra – whether the Fed can achieve this without further upending the broader economy.

So, does all this point towards the inevitability of a recession?

Let’s start with the basics.

What is a Recession?

Recessions are an unavoidable contraction in a nation’s economy, a natural part of the business cycle.

While many consider two consecutive quarters of declining GDP to be a recession, the non-partisan National Bureau of Economic Research (NBER) – the official arbiter of recessions – defines it slightly different.

According to NBER, “a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months” that manifests itself in the data tied to “industrial production, employment, real income, and wholesale-retail sales.”

Essentially three criteria that must be met to officially qualify as a recession: depth, diffusion, and duration.

What causes a recession?

Recessions can be set off in a variety of ways. Some causes include:

- Sudden economic shocks (1973 OPEC energy crisis)

- Bursting of asset/debt bubbles (‘01 dot-com bubble, ’08 subprime mortgage crisis)

- Too much inflation/deflation (US inflation in ‘70s, Japan deflation in ‘90s)

Is another recession inevitable?

It’s pretty much guaranteed, yes.

Since 1854 (the first year we have official economic data), the United States has experienced 35 recessions which have occurred, on average, nearly every 4-5 years.

A chart outlining some of these recessions (and their respective GDP contractions and durations) was featured in a blog post of ours from 2019 (also a timely read considering Le Tour just started!):

The Next Recession and What We Can Learn from the Tour de France.

Why do we care about recessions?

Recessions have real world consequences:

- Unemployment can rise: Recessions can lead to less spending/consumption which can result in layoffs, pay/benefit cuts, and heightened job insecurity. For job seekers, recessions can be a challenging time because there is less hiring and employees will typically have less leverage in pay negotiations.

- Businesses can fail: The same reduction in spending/consumption that leads to unemployment can also directly lead to businesses being forced into bankruptcy.

- Retirement plans can be upset: The retirement landscape is already full of landmines for the average American. Sprinkle in a recession + inflation and you have an environment that will be unforgiving to overspending/mistakes. Those that retain jobs may decide to stick around longer to weather the storm.

- Borrowing can get more difficult: As the broader economy slows down, or backtracks into recession territory, it’s not uncommon for lenders to tighten their standards for mortgages, vehicle financing, and other types of loans.

Is the United States heading for a recession?

It’s all opinion and speculation until it’s here. Poll various economists, strategists, and bankers and you will get inconsistent answers.

Even better yet – and perhaps just as reliable – ask your neighbor what they think. Consumer sentiment alone speaks volumes.

While recessions are hard to predict, leading indicators are pointing to the U.S. inching closer to one:

- 15% of US renters are behind on their payments

- U.S. homebuilding fell to a 13-month low

- Global factory growth/output has stalled

- S&P 500 had worst first half of year since 1970

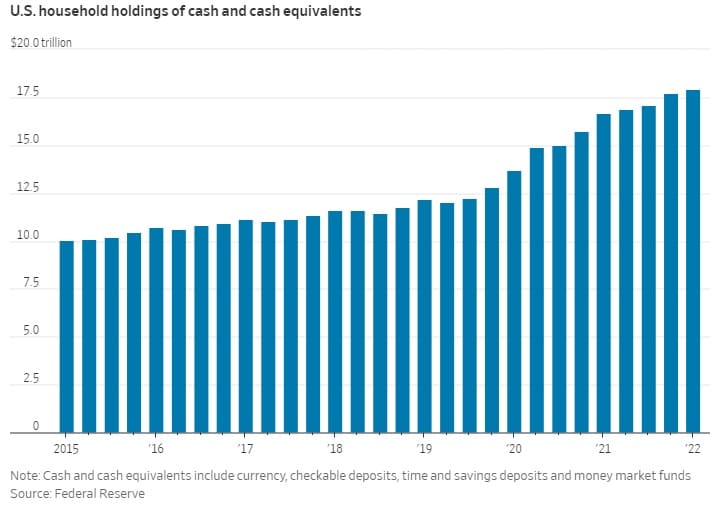

Room for optimism?

The consumer makes up 70% of the economy and there is an argument that, based on US household holdings of cash and cash equivalents, that the US consumer has never been more prepared for a slowdown:

And no, the cash is not necessarily being hoarded by just the wealthiest households. Those in the bottom half are holding 45% more cash than from two years earlier.

Growth in total household wealth also provides a glimmer of hope.

Between Q4 2019 and the end of Q1 2022, total household wealth increased from $109.9T to $141.1 T – an increase of nearly 30%. All this while the ratio of household debt to disposable income dropped to the lowest levels of anytime seen between 1980-2020.

Air flight – another indicator of consumer sentiment measured by TSA checkpoints – is also seeing it’s highest levels of passengers since the start of the pandemic. This is a great sign when considering that business travel is still down 30%.

Will this continue? Anyone’s guess. But at the moment the average US consumer has more cash, less debt, and more overall wealth than they’ve ever experienced.

Closing Thoughts:

The next time you hear the dreaded “R” word referenced, consider taking a page out of the Stoics’ playbook: prioritize the things within our control, and ignore the rest.

We have no way of knowing, or control over, when the economy will rebound, when inflation will subside, or when the market will be primed to recover it’s losses.

However, the things we can control include:

Financial:

- Spending habits (and potentially adjusting in light of inflation)

- Making strategic tax-planning decisions

- Paying down high interest debts

- Continuing to invest in the market.

Life:

- What we consume (food, media)

- Our mental and physical fitness

- Who we choose to spend time with

- The amount of sleep we get

- Our body language and breath

- Our opinions, attitudes, aspirations, dreams, desires, and goals.

- The number of times we smile, say “thank you,” or express gratitude for all we do have today

- Our level of honesty with self and others

In the words of Epictetus, “He is a wise man who does not grieve for the things which he has not, but rejoices for those which he has.”