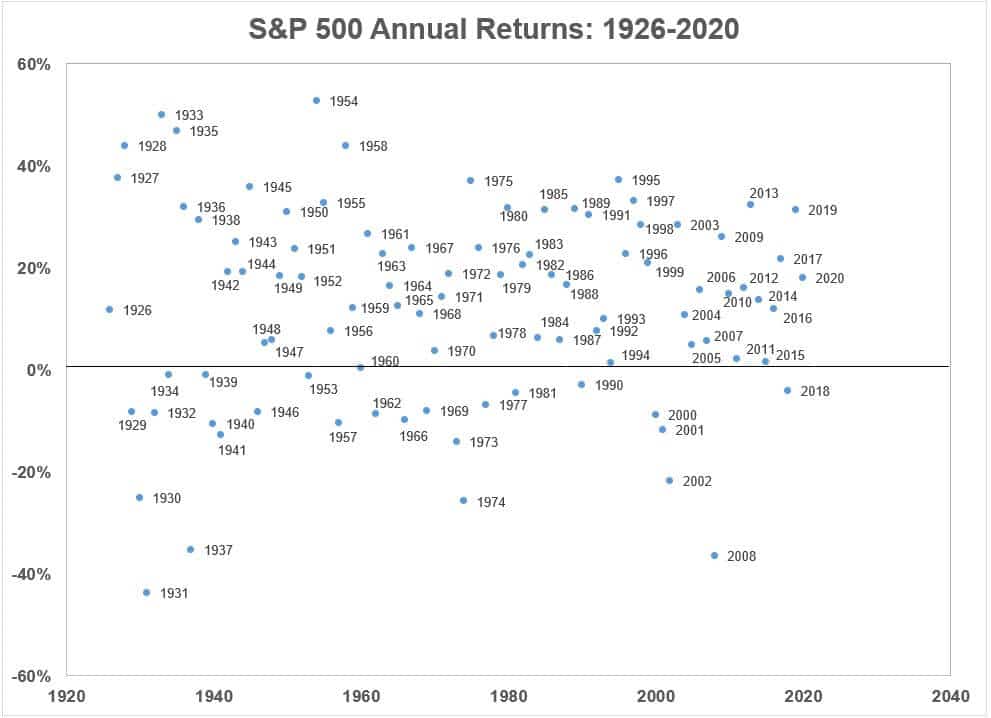

Between 1926-2020, the US stock market return was basically 10% per year.

While it’d be great to bank on 10% per year, it unfortunately does not work that way. For those that want consistency over the long haul, they will have to accept lower returns (think: CDs, bonds). For those that truly want higher returns over the long haul, they’ll have to accept more volatility (i.e. the stock market, other speculative investments). Either way, you can never fully escape risk.

Interestingly, though, is how infrequent annual US stock market returns actually fall within the long-term 10% average.

If we look at the calendar year returns +/- 2% from the 10% average (so 8% to 12%), this has happened in just five calendar years (1926-2020). So around 5% of all years since 1926 have seen what would be considered “average” returns. In fact, there have been just as many yearly returns above 40% as returns in the 8% to 12% range. Just 18% of returns have been between 5% to 15% in any given year.

The only way to truly take the randomness out of the stock market is to have a multi-decade time horizon. The best 30 year return was 13.6% per year from 1975-2004. And the worst 30 year return was 8.0% per year from 1929-1958.

What you can do about it:

It’s impossible to say if the next 30 years will be as kind to investors as the previous 30 were. For those that are still on the journey towards financial independence, it would be best to assume lower returns going forward. Instead of relying on continued 8-10%+ average annual returns (something beyond your control), personal savings and frugality are parts of the money equation that are more in your control and have a 100% chance of being as effective in the future as they are today.

As Morgan Housel, author of the “Psychology of Money” writes, “You can build wealth without a high income, but have no chance of building wealth without a high savings rates, it’s clear which one matters more.”