Written by: John Munley

My twin daughters got their first real jobs last summer, a common rite of passage through adolescence and good preparation for increased independence as they began their college adventure. I was a very proud parent. My kids would finally earn their own money and learn responsibility – or so I thought.

Little did I know at the time that my role and guidance as a parent was still very much needed.

When our children get that first paycheck and look aghast at the withholdings; that’s when we realize our kids know very little (or possibly, nothing) about how finances work. And maybe that shouldn’t be a surprise.

When something is provided to you automagically (like money for the movies or a new pair of yoga pants) you don’t need to know how it works. But when you’re the one holding the time card (and the debit card) it suddenly becomes super important.

If your kid is starting his or her first job this summer, you’ve got a great opportunity to talk with him or her about how we get paid and all the ways we could and should be spending those hard-earned dollars.

Here’s what to expect when your child works this summer.

Baby’s First W4 Form. You must be so proud.

After getting a job, the first thing that your teenager is most likely to bring you is a W-4 Tax Form. Employers use this form to withhold the proper amount of federal income tax from paychecks. The biggest challenge is deciding how many allowances to claim. The more allowances you claim, the less federal income tax your employer will withhold from your paycheck.

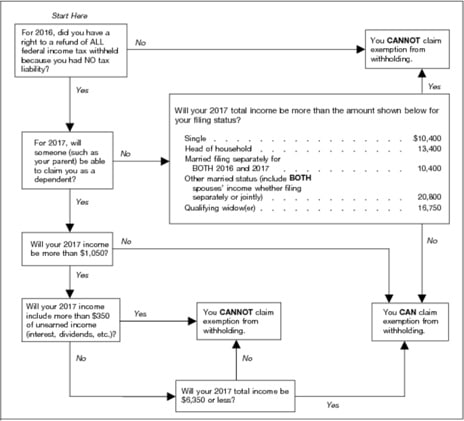

The first thing that you want to check is if your teenager is exempt from having Federal taxes withheld from her paycheck. The following chart published by the IRS will guide you to see if your child qualifies for exemption from withholding.

If your teenager does not qualify for exemption, then she must choose the number of personal allowances to claim. The Personal Allowances Worksheet consists of lines A through H and helps to calculate the allowances that your child should take. In most cases after filling out the worksheet, she will end up taking either zero or one allowance. With zero allowances, more federal taxes will be withheld which will lead to a larger refund at the end of the year. States may also have their own W-4’s which the employer may require.

The first paycheck. Where did all my money go?!

Your child gets a job for $10/hour and works 30 hours per week. When her first paycheck arrives, she’s shocked to learn that her total ‘take-home pay’ isn’t $300. You now get to explain the tax system and the difference between gross pay and net pay.

Use this as your basic script:

Gross is the amount earned based on salary and hours worked. Net is the actual take home pay after taxes are deducted. Everyone, regardless of age or income, has Social Security and Medicare taxes withheld from their paychecks which won’t be refunded when a tax return is filed. The Social Security tax counts towards your child’s earnings record, which is important as it’s used when determining her future benefits. If your child filed exempt on her W-4, no federal taxes are withdrawn. If she claimed zero or one, there will be federal taxes deducted from her earnings in addition to Social Security and Medicare. State taxes may also be deducted based on the state W-4 form that your child filled out.

Have fun laying all that out for her.

The double edged debit card.

How we pay for goods and services is an important decision that I don’t think we discuss as much as we should. Technology gives us multiple ways to pay for that new app or that concert ticket : debit cards, credit cards, checks, online payments, Venmo, Paypal, Apple Pay, etc.

Notice the one thing that I left out? Cash. The good old American dollar.

We live in a world where we hold less cash and increasingly use various cards and electronic payment methods. While paying electronically is convenient, there are some benefits when using cash.

First, we spend less when we use cash. Consumers are likely to spend more money using credit cards since it’s less painful than paying with cash. There is a separation in time between when the credit card is used to buy something and when the bill has to be paid, and this encourages us to be more impulsive spenders. With cash, we feel the pain of loss (our money!) immediately.

Second, not only do credit card users spend more, but they’re spending more money to instantly gratify unhealthy choices (read: donuts and caramel lattes).

Finally, those who pay with cash enjoy a better relationship with their purchased products and are more likely to have an emotional attachment with their purchase.

I’m a realist, and I recognize that in today’s world cash is no longer king. Most transactions are carried out electronically and – eventually – we may see cash as currency disappear completely. However, I think it’s important for teens to learn the value of cash. It is so easy moving money electronically from one place to another that it’s more like a videogame than a transaction.

It’s more painful to have to reach into your pocket or wallet and take out that $110 for the new pair of sneakers or $80 for the latest Xbox video game than it is to swipe a card or click the PayPal icon. When paying with cash, you think hard about the purchase you’re making. With credit cards and other electronic payment choices, you can buy it now and worry about the impact on your net worth later.

I encourage my twins to make half of their purchases using cash. While the paper U.S. dollar exists, I want them to think hard about the purchases they make, and hopefully prevent them from building up debt or spending more than they have.

Saving for retirement (even though they’re totally never going to be that old).

One of the most important things your child can do at this early stage in their working lives is learn to save. I will tell you now that the last thing your kids want to hear is that they should begin putting money aside for retirement. The 45 to 50 years between the halcyon days of youth and when retirement will start for your child may as well be a million years away to them. However, the fact is that most Americans are not saving enough to maintain their standard of living in retirement.

Teaching our kids – now – the importance of setting money aside will pay huge dividends for them down the road. The most important reason to start saving now is the power of compounding, or the accumulation of extra money on the interest/gains received from investments. The more you invest and the earlier you start means your savings will have that much more time and potential to grow.

One of the best ways to start your child saving is through a Roth IRA. To contribute, you only need earned income from a job. Up to $5,500 can be contributed each year, and the contributions can be withdrawn tax-free and penalty-free at any age. After age 59 ½, the earnings can also be withdrawn tax-free.

Here’s a thought, tell your son or daughter that if they save $50 from every paycheck toward their future you’ll match it dollar for dollar.

The hard lesson: You can’t buy everything you want (but you can buy some big stuff later).

Now that your teenager is earning her own money, I’m sure she’s thinking about the numerous ways she can spend it. Now is a great time to introduce the concept of budgeting. And you can do this without a spreadsheet.

Your ultimate goal is to teach your kid how to achieve a balance between money coming in and money going out.

The first thing to do is to sit down with these spenders and clarify what you will pay for and what they are responsible for. This is especially important with college age kids. (My girls were shocked to learn I wasn’t going to pay for spring break.) Are they responsible for paying part of their tuition? Books? Social events? Meals?

You can do the same with high school kids as appropriate. Do they have to pay for any of their clothes or entertainment or meals with friends? This is your baseline for a spending plan. (Maybe we don’t say to our kids “budget” lest they think we’re cramping their new found ability to make it rain at Applebee’s.)

Help your teenager write down the income she’ll earn this year and all the known expenses she’ll be responsible for. After accounting for expenses, your child should come up with a list of goals she wants to achieve – buy a new computer, a fancy phone upgrade, maybe even a car. Now she’ll have a good understanding of how much money she needs to save to get there. And you might just get to keep some of your hard earned cash.