Written by: John Munley

Last week, I shared some advice I want to gift to my young daughters about establishing good financial habits, early. My inspiration was a speech the principal at my daughter’s school gave during her moving up ceremony. I was especially moved by a quote by Kid President about The Path to Awesome.

This week, my focus is on some of the nitty-gritty specifics of early investing strategies because the money we earn (or receive as gifts) really can continue to grow with us — if we take even a few hours to learn more about some simple principles and investment tools. And this IS important (and I hope my daughters are listening!), because the earlier we begin using these principles and tools, the more money our investments will earn and the more freedom and options we’ll have as we travel on our path to awesome.

As we consider what will best serve our goals to build a solid financial future, remember that in order to accomplish these goals, we’re going to need three things: Awareness, Courage and Knowledge. We need these because, as with most decisions in life that have the potential to significantly propel us forward towards our goals, success depends on being aware of our feelings, thoughts, desires and fears about the goal; having the courage to take action and respond to the consequences of those actions, and acquiring the knowledge necessary to make the best possible decisions in the first place.

Depositing all your money in a traditional savings account is certainly one option for investing your money, and in some cases, it’s a great idea. But is it the best idea for building financial assets for the long-term?

Here’s an unambiguous answer — No. And here’s why.

#1: The Magic of Compound Interest

I am sure you have heard of the term compounding before but may not be sure exactly what it is. The easiest explanation — compounding means you are earning interest on your interest.

For example, let’s say you have $100 in an investment account and are earning 7% per year in interest. After your first year, you will have $107 in that account. In the second year, you will not only be earning interest on the original $100 but also on the $7 of interest you earned in the first year.

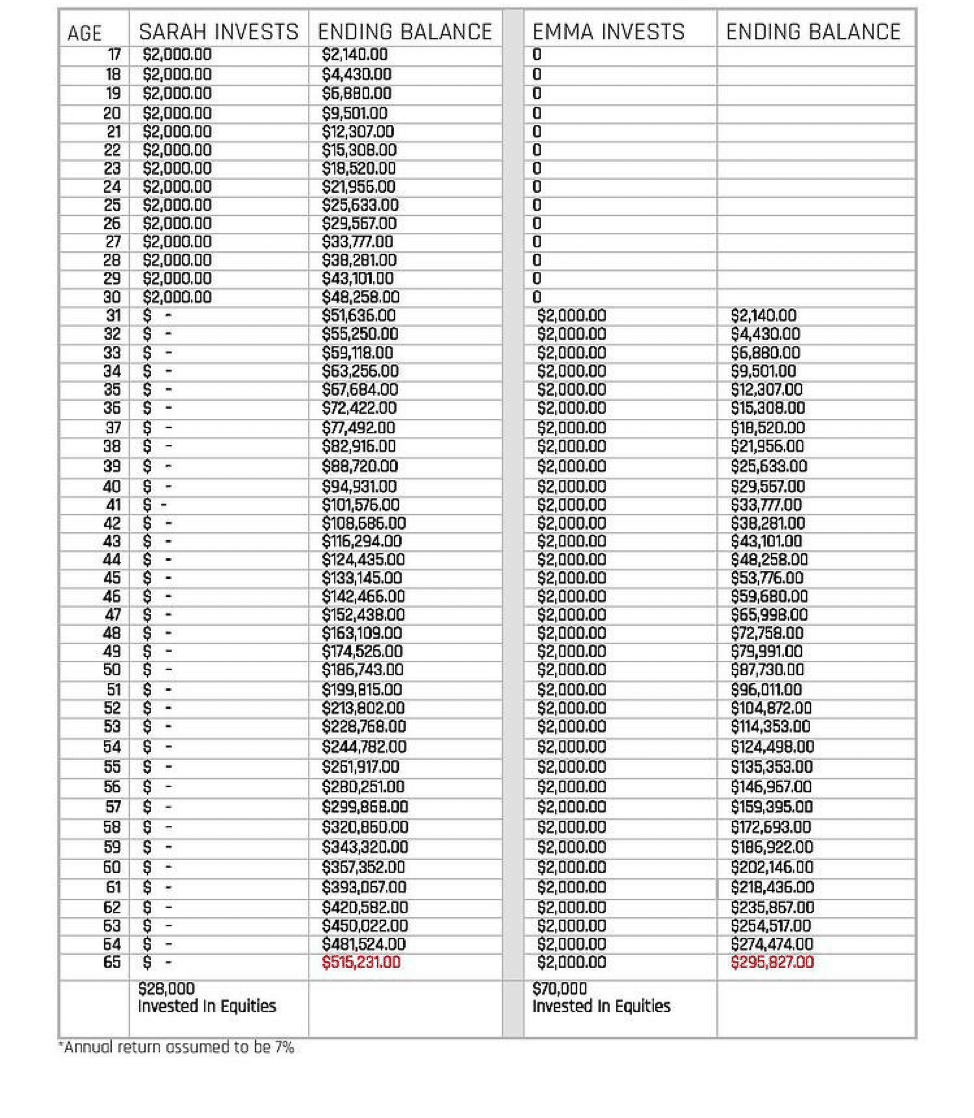

You’ve probably heard, repeatedly, about the benefits of starting to save at an early age — the earlier the better. Compound interest is the reason for this. Taking advantage of compounding is sound financial advice at any age, but the younger you are when you start saving, the longer your money has to grow. And the longer your time horizon, the more easily you can bounce along with the fluctuations in the equity markets.

I gave an example of compounding in my last blog. There, I was using it to prove my point that the earlier we begin saving, the more money we’ll have down the road, but it’s also a great example of the magic of compounding. Here’s a quick peek at how that works laid out in a neat little chart:

#2: Risk and Reward: How Courage and Knowledge Pay Off

You have worked hard for that paycheck. You’ve set a goal for yourself to build your savings early and to give yourself the most options along your path to awesome.

Now, the question becomes how to invest that money so that it can do the job you need it to.

We just learned why compounding is the real-world magic we need. How best to wield it? Not through parking our money in a saving account, so how?

There are a (mind-boggling) host of investing options that come with various degrees of risk and return and, in general, the lower the risk, the lower the return will be. A savings account is certainly the least risky, but your return is also lower than with other options. The important thing to remember is that there is not just one right investment strategy and there are no get rich quick schemes.

In my opinion, though, the fact that you or your child is starting early (and if not early — let’s give ourselves a thumbs up for beginning today!) is the most important factor in reaching your goal. Let’s take this example: you graduate college and your new employer gives you a $10,000 sign on bonus. It would be very tempting to throw a party for you and your friends, or go out and spend that money on cool, self-congratulatory swag (but first you would remember the obvious taxes due – about $3,245 of them when you consider statutory federal and state tax withholding requirements, Medicare tax, and Social Security tax…so your $10,000 party would really only be $6,755 party).

But, being the wise person that you are, you remember from reading the earlier blog, So You Teenager Got Her First Job – Now What?, that most Americans are not saving enough to maintain their standard of living in retirement. So instead of blowing that tidy sum, you save it. Depending on your goals, maybe you save all of it. I can tell you that if you are serious about financial freedom, saving the bonus into your new company’s 401k plan allows you to keep the whole $10k instead of netting only $6755 after tax as we discussed above.

Here’s where knowledge about personal finance is a most valuable asset. Take the time to learn why and how money can be a great tool to help you reach your biggest, most cherished goals. Community colleges often offer personal finance classes for reasonable tuition that will give you a good understanding of basic vocabulary and principles. Bottom line, the more you know, the better your decision-making.

For the sake of this example though, let’s keep it simple and compare your return on investment in two different scenarios: 1. Deposit your bonus in a traditional savings account (ie: Park and Ride), and 2. Invest your bonus in the stock market (Knowledge + Courage).

In scenario 1, if you simply dropped it into a savings account, you would only be starting off with $6,755 (remember those darn taxes) and based on the average historical rate of return for a traditional savings account (about 4.5% since 1954), after 43 years you could expect to have a total balance of $44,063. This savings rate would have resulted $37,308 of earnings over that time.

In scenario 2, you instead elect to save your bonus into your 401k. This gets you the full $10,000 (defer those taxes!) to invest. If we assume the long term average return of a moderate portfolio (made up of 60% in stocks and 40% in interest earning assets), saving that $10,000 bonus at the age of 22 into the a tax efficient, diversified investment portfolio would turn into $361,302 by the time you reached the age of 65. Now how many parties can you throw with that??! There’s that good old magic of compounding interest at work for you!

#3: Short Term Goals: When the Right Decision Means Spending NOW

Now, not all of your money should necessarily go into the equity market. After all, we need to grow and build and live and enjoy life along the way to retirement, right? Life is happening every day between here and retirement!

For our important short term goals such as traveling, a downpayment for a house, or purchasing a car, we want to keep our money safe and away from the volatility of the equity market and, more accessible. We want to make sure that money is readily available when you need it, so leaving a portion of your money assets in a savings account or other lower-risk investment is a great idea.

How much should you put into a straight savings account? I tell my daughters between 10% and 15%. As you see your income and your balances grow and you see your goals and aspirations develop, you may decide to rebalance this percentage.

Then, as you see your investments grow and start meeting some of those early goals — you’ll likely want to start working with a trusted financial life guide, someone who has expertise in not only how to save and invest but who also has a wealth of experience from helping others succeed…and lessons learned from other people’s mistakes.

Together, you can employ self-awareness, courage and knowledge to make sure you’re on the right path to awesome.